Buying your first home is a huge milestone in one’s lifetime. The experience is exciting, but it can also be nerve racking since it is such a large asset. Because your home will most likely be your biggest financial asset, it’s important to make sure you, your home and your belongings are protected.

Top tips for first time home insurance buyers

Purchasing your first homeowners insurance policy may feel like an overwhelming experience, but it doesn’t have to be. At Indiana Farm Bureau Insurance, we can help walk you through the process and help you create a policy you can rely on.

1. How much coverage do I need?

If you aren’t quite sure how much coverage you need for your home, that’s okay. Your insurance agent can guide you through this. When walking through the process, you will want to make sure you have enough insurance to cover the cost to rebuild your home, which may be more than your purchase price.

2. What does the home insurance policy cover, and what type of policy is it?

There is no such thing as a one-size-fits-all-home insurance policy. There are two main types of policies for owner-occupied dwellings. One is an HO-2 policy. This policy outlines 16 very specific perils that are covered. A peril is an event that causes damage to your home or property. The second is called an HO-3 policy, which can cover specific losses unless they are excluded from the policy. The best way to know what is and is not covered by your home insurance policy is by asking your agent.

3. Pay attention to deductibles.

A deductible is the amount of money you will have to pay before the insurance will pay any claims. The higher your deductible, the lower your insurance premiums will be, but the more risk you take on. The most common deductibles are between $1,000 and $2,500 on home insurance policies. But remember, these numbers can be adjusted, based on your preferences and the amount of coverage you feel comfortable having in place.

4. What should my liability limits be?

The industry standard liability limit is $300,000; however, if you have a pool, you should consider increasing your liability coverage to $1,000,000 to cover legal and medical expenses in the event of a pool-related accident.

5. Indiana Farm Bureau Insurance discounts

Indiana Farm Bureau Insurance offers multiple discounts for customers wanting to save on their insurance policies. One discount that everyone should take advantage of is the Multi-Line Discount. If you purchase both your auto and home or auto and renters insurance policies at Indiana Farm Bureau Insurance, you can save up to 23% on your insurance premiums.*

6. What are endorsements?

Endorsements are like going through an à la carte line. This is where you customize your policy to fit your lifestyle and geographical location. Some big ones in Southern Indiana include:

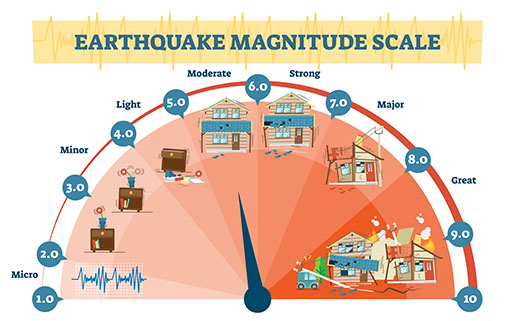

- Earthquake coverage - People who live in southwestern Indiana sit on the New Madrid Fault line. This fault line is capable of a 7.0 magnitude earthquake. Earthquake coverage has a separate deductible from your home insurance policy. The earthquake endorsement can have a 5%, 10% or even a 20% deductible depending on what you choose. To figure out what that means in dollars for you, take your dwelling Coverage A and multiply it by one of the above percentages.

Coal mine subsidence coverage - "Mine Subsidence" means lateral or vertical ground movement caused by a failure initiated at the mine level, of man-made underground mines, including, but not limited to coal mines, clay mines, limestone mines and fluorspar mines that directly damages residences or commercial buildings. In simpler terms, when the roof of a subsurface mine collapses, it causes the ground above to sink or subside.” - IMSIF

To get an idea if your home was built over a mine, please visit the DNR Coal Mine Information System.

If you are buying a home in southwestern Indiana, especially in counties such as Warrick and Gibson, I strongly suggest you look at this map and add the endorsement if necessary.

Sump pump and water back up coverage - If you have a sump pump in your basement or crawlspace, you need this coverage. This can help cover clean-up, which can cost thousands of dollars, dry out and replacement of materials. Certain parts of some towns really struggle with water backing up into people’s homes. The water back up portion of this coverage will cover water backing up into your home or water backing up into a shower or toilet.

Make buying home insurance for the first time simple. Let’s start the conversation, today!

Graphic Credit: VectorMine - stock.adobe.com

*Talk to an Indiana Farm Bureau Insurance agent for more information on discounts

Inside Story is for educational and informational

purposes only. Inside Story is compiled from various sources, which may or may

not be affiliated with our family of companies, and may include the assistance

of artificial intelligence. While we strive to provide accurate and reliable

content, we make no warranties or guarantees about its completeness, accuracy,

or reliability, and are not responsible for the content of any third-party

sources or websites referenced herein. The inclusion of any content does not

establish a business relationship or constitute our endorsement, approval, or

recommendation of any third party. Testimonials and examples provided are for

illustrative purposes only and do not guarantee future or similar results or

outcomes, and may not consider individual circumstances, goals, needs, or

objectives. Inside Story does not provide legal, tax, or accounting advice. For

individual guidance, please consult a qualified professional in the appropriate

field.

Coverages

subject to policy terms, conditions, and exclusions. Subject to underwriting

review and approval.